All Categories

Featured

Table of Contents

It's vital to keep in mind that your cash is not directly purchased the securities market. You can take cash from your IUL anytime, yet costs and give up costs might be related to doing so. If you require to access the funds in your IUL plan, weighing the advantages and disadvantages of a withdrawal or a loan is necessary.

Unlike direct financial investments in the stock exchange, your cash money value is not straight bought the underlying index. Understanding Indexed Universal Life Insurance (IUL) vs. Roth IRA. Instead, the insurer uses financial tools like alternatives to connect your cash money value development to the index's performance. One of the one-of-a-kind functions of IUL is the cap and floor prices

Upon the insurance policy holder's fatality, the beneficiaries obtain the death benefit, which is normally tax-free. The survivor benefit can be a set quantity or can include the cash value, depending on the plan's framework. The money value in an IUL policy expands on a tax-deferred basis. This implies you do not pay taxes on the after-tax resources gains as long as the cash stays in the policy.

Always evaluate the policy's details and seek advice from with an insurance coverage specialist to completely comprehend the advantages, limitations, and costs. An Indexed Universal Life insurance policy plan (IUL) supplies a special mix of functions that can make it an eye-catching choice for specific people. Here are several of the crucial advantages:: Among one of the most appealing elements of IUL is the possibility for higher returns compared to other sorts of irreversible life insurance policy.

Taking out or taking a funding from your policy might reduce its money worth, survivor benefit, and have tax obligation implications.: For those curious about legacy preparation, IUL can be structured to supply a tax-efficient method to pass riches to the next generation. The fatality advantage can cover inheritance tax, and the cash value can be an extra inheritance.

How Does A Roth Ira Compare To Iul For Retirement Savings?

While Indexed Universal Life Insurance Policy (IUL) supplies a series of benefits, it's vital to think about the potential drawbacks to make an informed choice. Right here are several of the key drawbacks: IUL plans are much more intricate than traditional term life insurance plans or entire life insurance plans. Understanding just how the cash worth is linked to a supply market index and the implications of cap and flooring prices can be challenging for the average consumer.

The premiums cover not only the expense of the insurance coverage however likewise administrative charges and the financial investment element, making it a more expensive alternative. While the cash value has the possibility for growth based upon a stock exchange index, that growth is frequently topped. If the index does incredibly well in a provided year, your gains will certainly be restricted to the cap rate defined in your policy.

: Including optional attributes or bikers can enhance the cost.: Exactly how the plan is structured, consisting of exactly how the cash money value is designated, can additionally influence the cost.: Various insurance firms have various rates models, so shopping around is wise.: These are fees for managing the plan and are generally subtracted from the cash money value.

Pros And Cons Of Iul

: The prices can be similar, yet IUL uses a floor to help shield versus market slumps, which variable life insurance policy plans typically do not. It isn't simple to provide an exact expense without a specific quote, as rates can vary considerably in between insurance companies and individual circumstances. It's essential to stabilize the importance of life insurance policy and the requirement for included security it provides with possibly higher costs.

They can help you comprehend the prices and whether an IUL policy straightens with your monetary objectives and requirements. Whether Indexed Universal Life Insurance (IUL) is "worth it" is subjective and depends on your monetary objectives, danger tolerance, and long-term preparation needs. Right here are some points to take into consideration:: If you're trying to find a long-term investment lorry that offers a death benefit, IUL can be an excellent option.

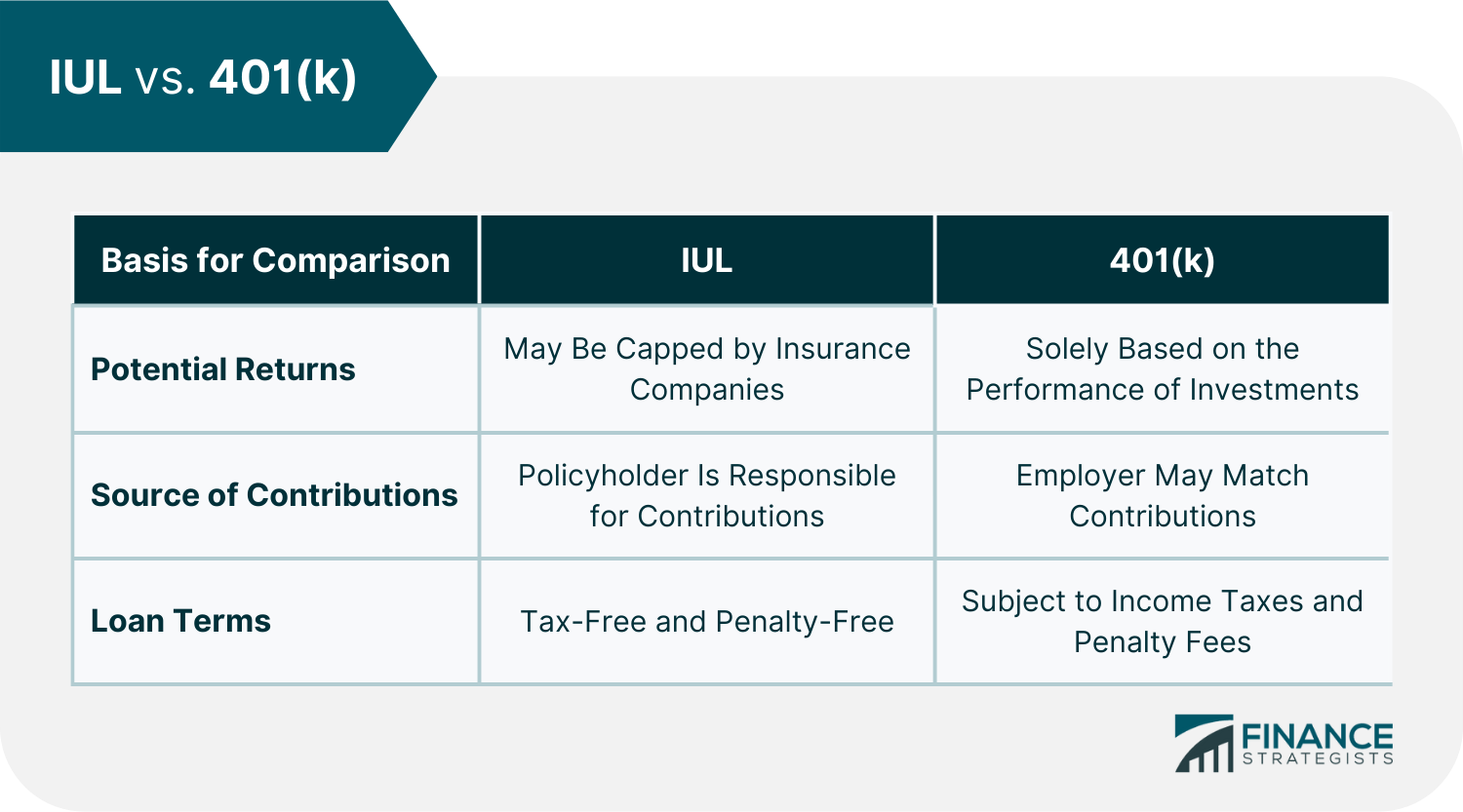

(IUL) policy. Comprehending the difference between IUL vs. 401(k) will certainly help you intend efficiently for retired life and your family members's financial health.

Indexed Universal Life Insurance Vs Retirement Accounts

In this situation, all withdrawals are tax-free given that you've already paid taxes on that income. When you pass away, the funds in your 401(k) account will certainly be moved to your recipient. If you do not designate a recipient, the cash in your account will enter into your to settle any kind of impressive financial debt.

You can grow your Roth IRA account and leave all the cash to your beneficiaries. Additionally, Roth IRAs offer even more financial investment choices than Roth 401(k) strategies. However, your only alternatives on a Roth 401(k) strategy are those used by your strategy carrier with.The downside of a Roth individual retirement account is that there's a revenue limitation on that can contribute to an account.

This isn't a function of a Roth individual retirement account. Because 401(k) strategies and Index Universal Life insurance policy function in different ways, your savings for each and every depend upon special variables. When contrasting IUL vs. 401(k), the primary step is to comprehend the overall purpose of retired life funds contrasted to insurance benefits. Your retirement funds need to have the ability to maintain you (and your spouse or family) for a couple of years after you quit working.

You should approximate your retired life needs based upon your existing earnings and the standard of living you intend to maintain throughout your retirement. Generally, the cost of living increases every two decades. You can use this inflation calculator for even more exact results. If you discover 80% of your current annual income and increase that by 2, you'll get a price quote of the amount you'll require to endure if you retire within the following 20 years.

We intend to introduce below to make the estimation less complicated. If you take out about 4% of your retirement earnings each year (considering inflation), the funds need to last concerning three decades. As a matter of fact, when comparing IUL vs. 401(k), the worth of your Index Universal Life Insurance plan depends on variables such as; Your existing earnings; The approximated cost of your funeral service expenditures; The dimension of your household; and The earnings streams in your home (whether somebody else is used or otherwise). The even more recipients you want to support, the even more money needs to go towards your death advantages.

Indexed Universal Life Insurance Vs. Qualified Retirement Plans (401(k)/ira)

Actually, you do not have much control over their allotment. The primary function of long-term life insurance coverage is to provide additional financial backing for your household after you pass away. You can withdraw money from your money value account for personal demands, your insurance coverage provider will certainly deduct that amount from your death advantages.

You can have both an Index Universal Life Insurance coverage policy and a 401(k) retirement account. You must understand that the terms of these policies transform every year.

Prepared to get going? We're below for you! Book a totally free examination with me now!.?.!! I'll respond to all your concerns about Index Universal Life Insurance Policy and how you can achieve wealth prior to retired life.

{kind=link}

Latest Posts

Guaranteed Universal Life Insurance Cost

Smart Universal Life Insurance

No Lapse Universal Life Insurance